As I grow my practice, more people are reaching out with questions about retiring early. What’s interesting is that almost no two people mean the same thing when they say “early retirement.” For some, it means leaving work entirely. For others, it means scaling back, changing careers, or simply knowing they could stop if they wanted to.

While the destination often sounds similar, the path to get there looks very different. That said, after reviewing hundreds of cases over the last several years, I’ve noticed consistent patterns among people who actually make early retirement work, not just in theory, but in real life.

Today I want to share what I see most often. These are common characteristics of early retirees and in some cases, you may already be closer than you think.

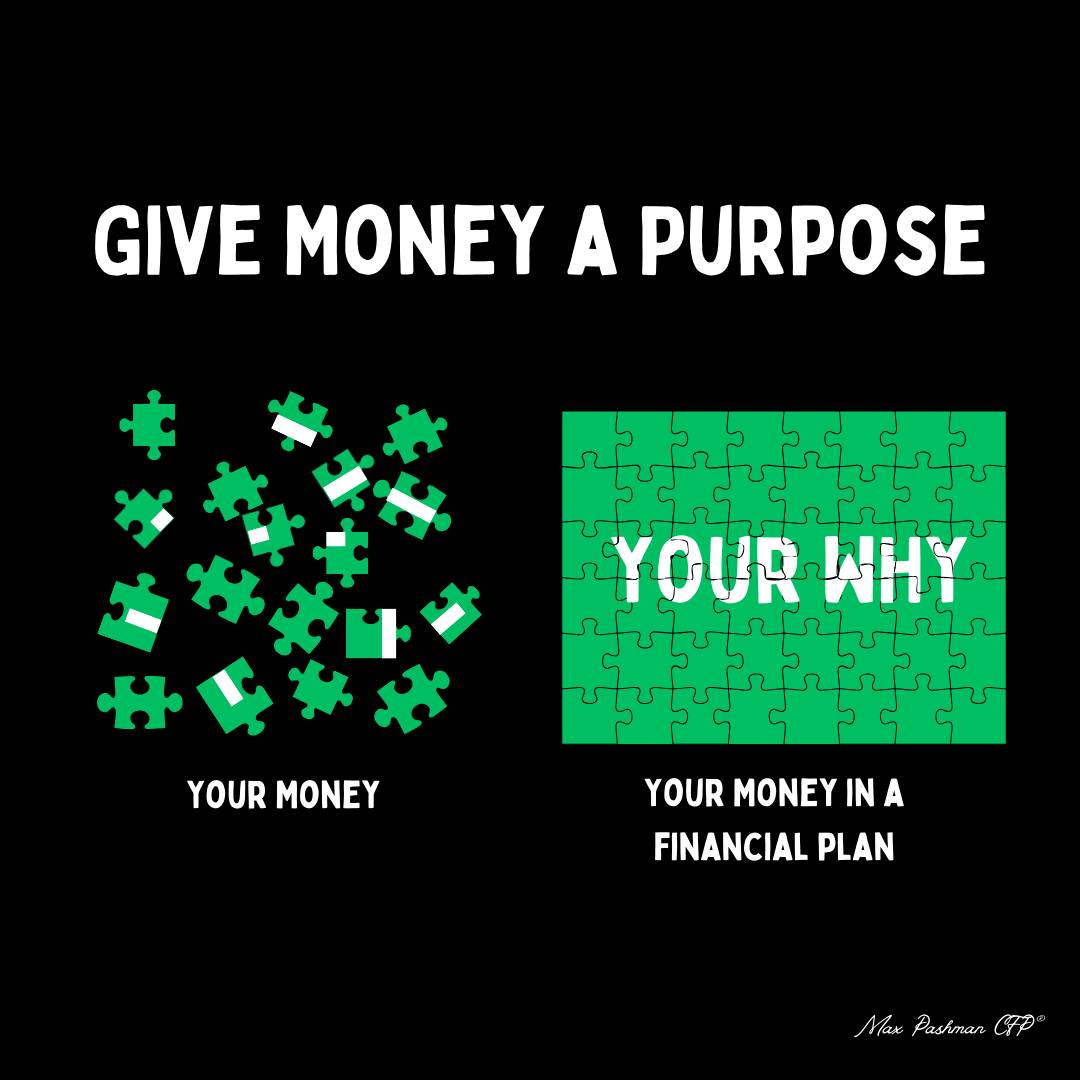

When money is tight, the primary goal is earning more of it. Once someone has enough, the focus shifts. The goal becomes finding meaning that does not revolve around money itself. Many people think early retirement is simply about building wealth, but those who succeed usually have a much clearer reason behind it. Whether it’s spending more time with family, working on a passion, starting a new venture, or having control over their time, purpose gives the plan direction. Once that purpose is defined, saving and staying consistent become easier, especially during periods when motivation is tested.

High income plays a significant role, and there is no real way around that. Many people believe budgeting alone will get them to early retirement, and while that is possible, it is not the most common path I see among highly compensated professionals or business owners. Expenses can only be reduced so far, but income has a much higher ceiling. Higher income creates more cash flow, and that excess cash flow is what allows wealth to be built and compounded more quickly.

High income alone is not enough if spending grows just as fast. That said, early retirees are not necessarily extreme savers either. Their spending is best described as reasonable, meaning it aligns with their values and long-term goals. They are intentional about what they are willing to spend on and equally clear about what does not matter to them. Once those priorities are established, the tradeoffs become easier to make and far less emotional.

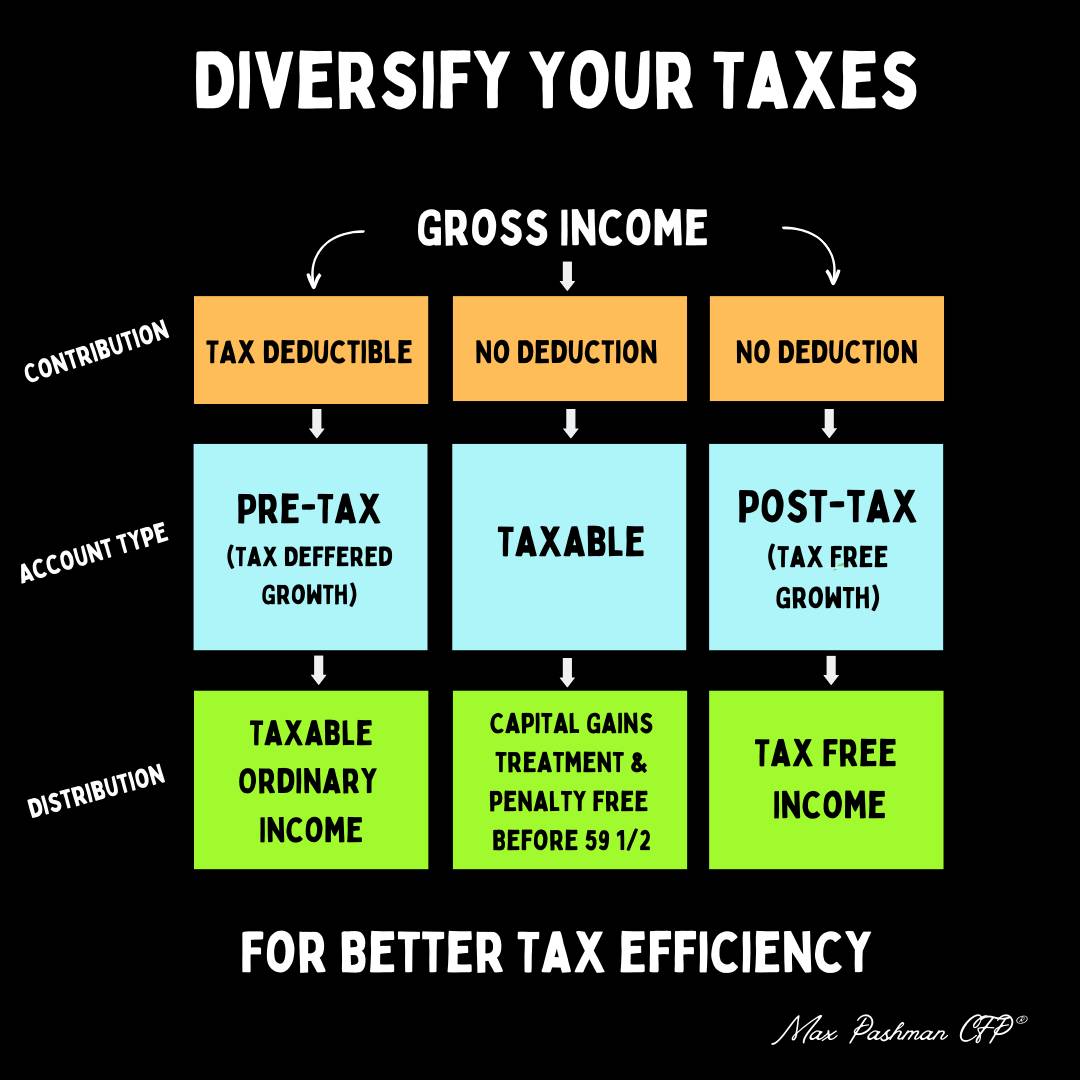

There is no single account or product that does everything well, despite how often that idea is marketed. Wealth works best when it is spread across multiple strategies that each serve a purpose. Different accounts provide different benefits related to access, taxes, growth, and flexibility. Having multiple options reduces stress and gives people more control over how and when they use their money.

This is more of a mindset than a skill. People who retire early are generally willing to look directly at their numbers. They know where their money is, understand their cash flow, and have a realistic sense of their financial position. What they usually want help with is not awareness, but confirmation. They want to know whether their instincts are right and whether there are blind spots they may be missing.

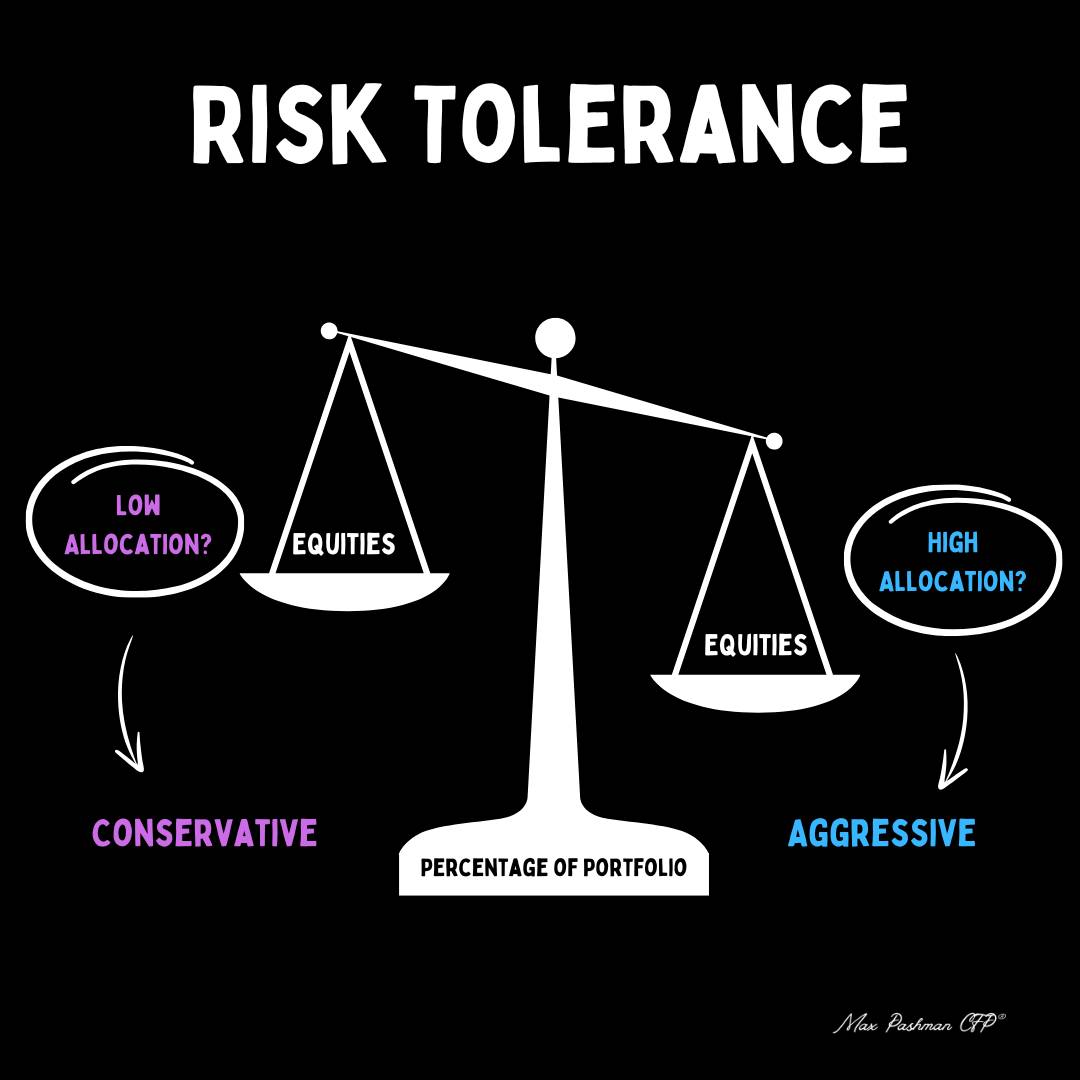

Traditional retirement models often assume someone in their 60s with a shorter time horizon and higher near-term spending needs. Early retirees typically do not fit that profile. They often have longer timelines, more flexibility, and the ability to adapt if things change. As a result, they are usually more comfortable taking on higher investment risk, particularly through equities. This requires different planning assumptions and a more intentional approach than the standard retiree model.

Most early retirees do not stop working entirely. Some continue because they enjoy it, others because it provides benefits or structure, and some because it offers supplemental income. The key difference is that the work becomes optional. They have the ability to slow down, pivot, or stop altogether. That flexibility is often the real goal of early retirement, not the absence of work.

There are many ways people reach early retirement, but three paths show up most often: building a successful business, benefiting from equity at a growing company, or maintaining a very high savings rate over time. In each case, ownership plays a major role. While stocks are often a significant driver of growth, early retirees tend to reduce concentration as financial independence approaches. They still rely on equities for long-term growth, but they avoid putting all of their outcomes in one place.

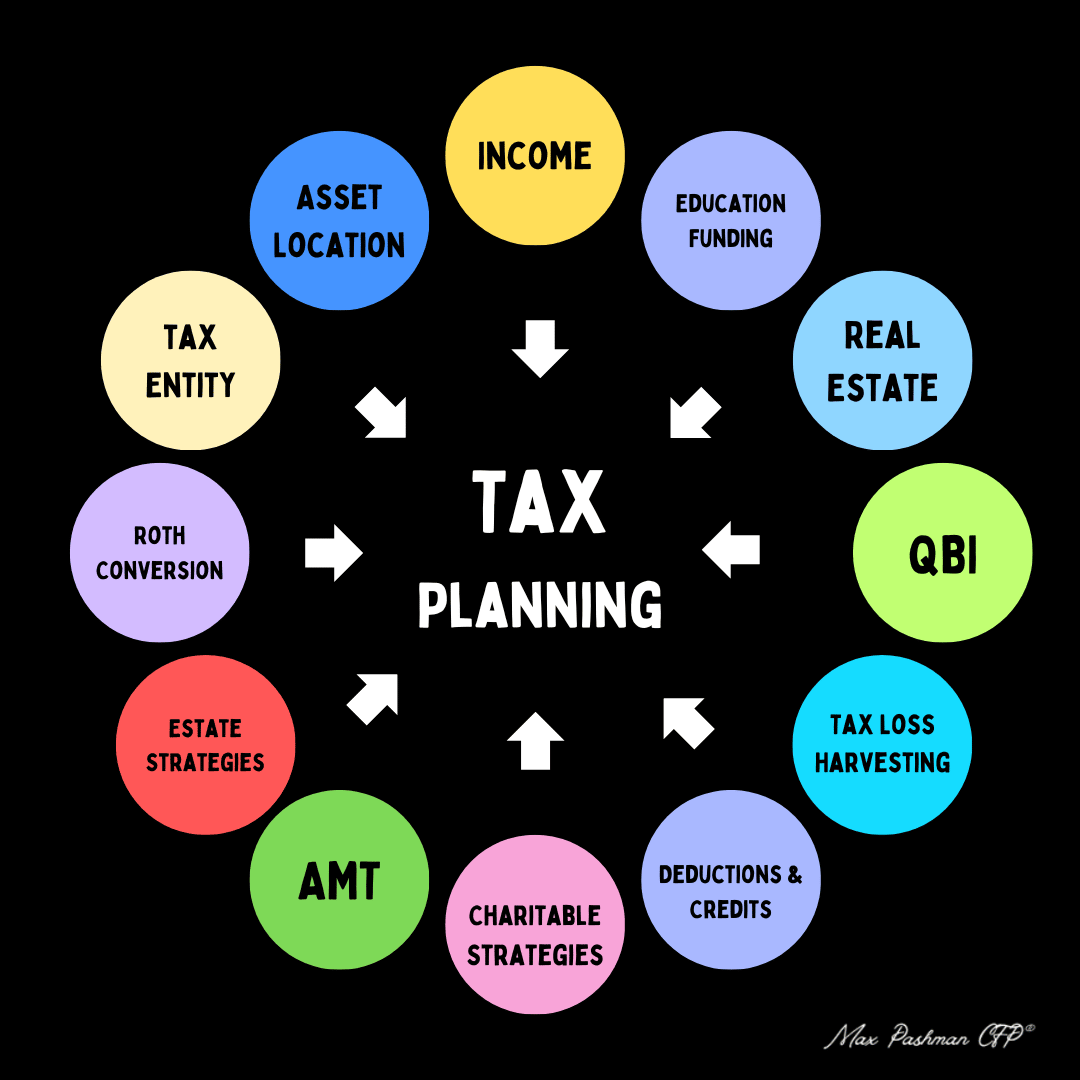

Building wealth is important, but tax planning often determines how long that wealth lasts. Thoughtful strategies around tax location, asset location, Roth conversions, loss harvesting, and distribution sequencing can meaningfully extend a retirement timeline. In many cases, proper tax planning adds years of flexibility that would not exist otherwise.

Even confident and capable people have blind spots. At some point, the goal shifts from feeling mostly confident to being fully prepared. A second opinion can provide validation, identify risks, and clarify tradeoffs that are easy to miss when planning in isolation.

Early retirement is rarely a solo effort. It’s a process of refining assumptions, stress-testing decisions, and understanding the tradeoffs before they matter. The people who do this well are not chasing perfection; they are building flexibility and choice.

And in the end, that’s what early retirement is really about.

Need help with your financial planning? Let’s chat and talk more about how we can help elevate your financial situation! Book a call here.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.