You join a company. Get equity. And after the company does well, you are rewarded for it. The stock grows. Your net worth grows. And before you realize it, a large portion of your financial life is tied to one position.

On paper, that feels like a win. And to be fair, it is.

But here’s where things quietly shift. Your income is tied to the company. Your career is tied to the company. Your benefits are tied to the company. And now your portfolio is heavily tied to the same outcome. That’s not diversification. That’s concentration layered on top of itself.

So the real question isn’t whether the company is good or bad. It's understanding how much exposure you want towards it. And most of the time, people are looking for ways to reduce that concentration.

But more importantly, it's about reducing that risk without creating an unnecessary tax burden along the way. Here we’re going to dive into some of the top ways we see tech employees do so tax efficiently.

Most people assume that selling means getting hit with a large tax bill, so they avoid doing anything at all. But this is the truth:

Paying taxes is likely the price you're going to pay one way or another. The question is just a matter of how you do it. Manaing your concentration relative to capital gains is an example of this.

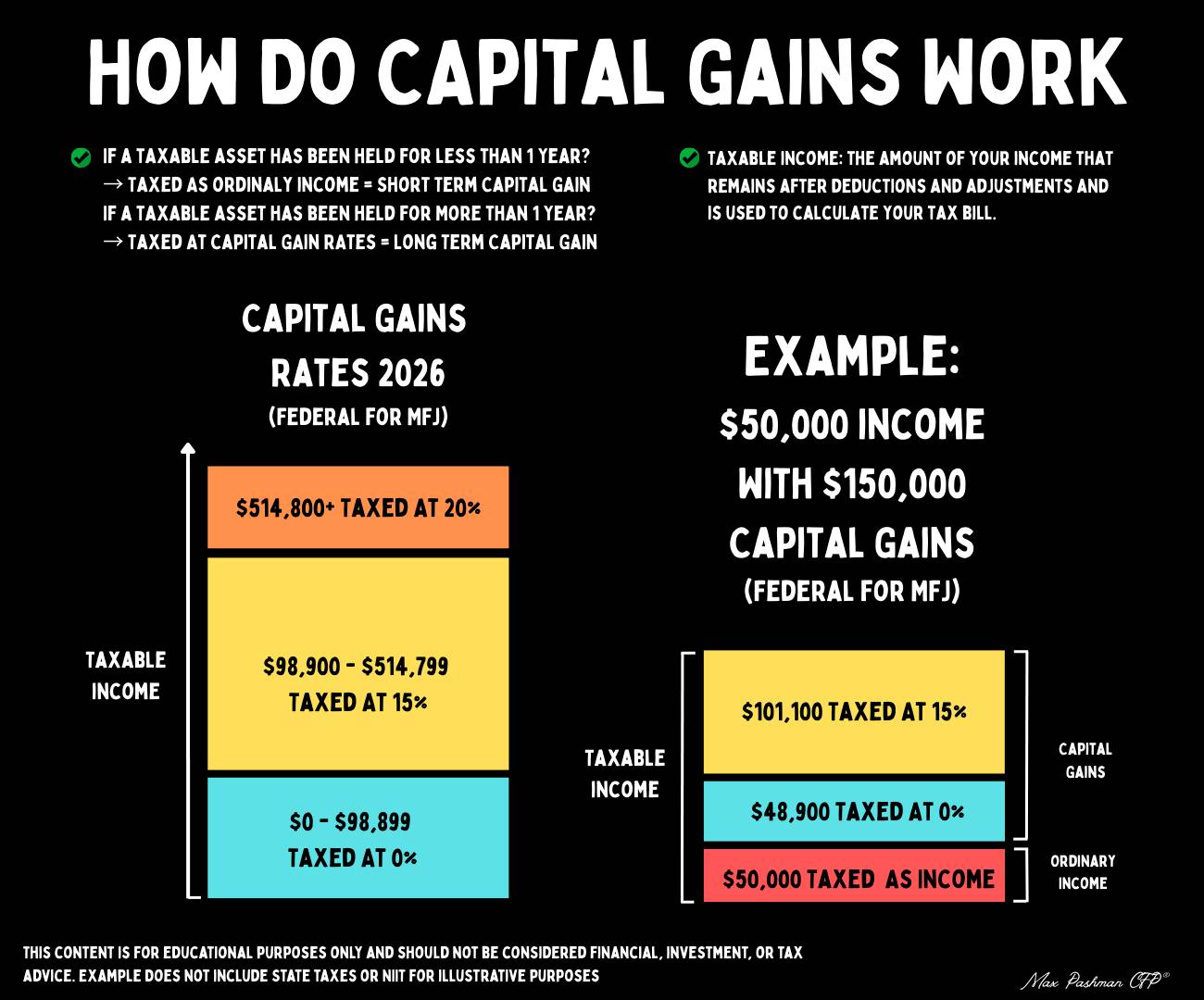

As a reminder, there are two ways your taxable assets get realized. Short term is when it's held less than a year and is then subject to ordinary income. Long term is when it's held more than one year and is then subject to capitl gains rates, which are most of the time more preferential.

There are ranges where gains can be taxed at 0% federally, and broader ranges where you can stay within the 15% bracket. The opportunity here is not to eliminate taxes entirely, but to be intentional about when and how much you realize.

This becomes especially relevant in years when your income is lower than usual. Early retirement is a common example, but it can also apply in transition periods between jobs or after a major liquidity event.

Instead of selling everything at once, the strategy becomes more about pacing. You gradually reduce exposure over multiple years, filling up lower tax brackets without spilling into higher ones. That being said, the longer you hold the longer risk you are still participating in, so that must be a factor.

It’s less about timing the market and more about managing the tax impact over time. This is important to remember as you trim your position over time.

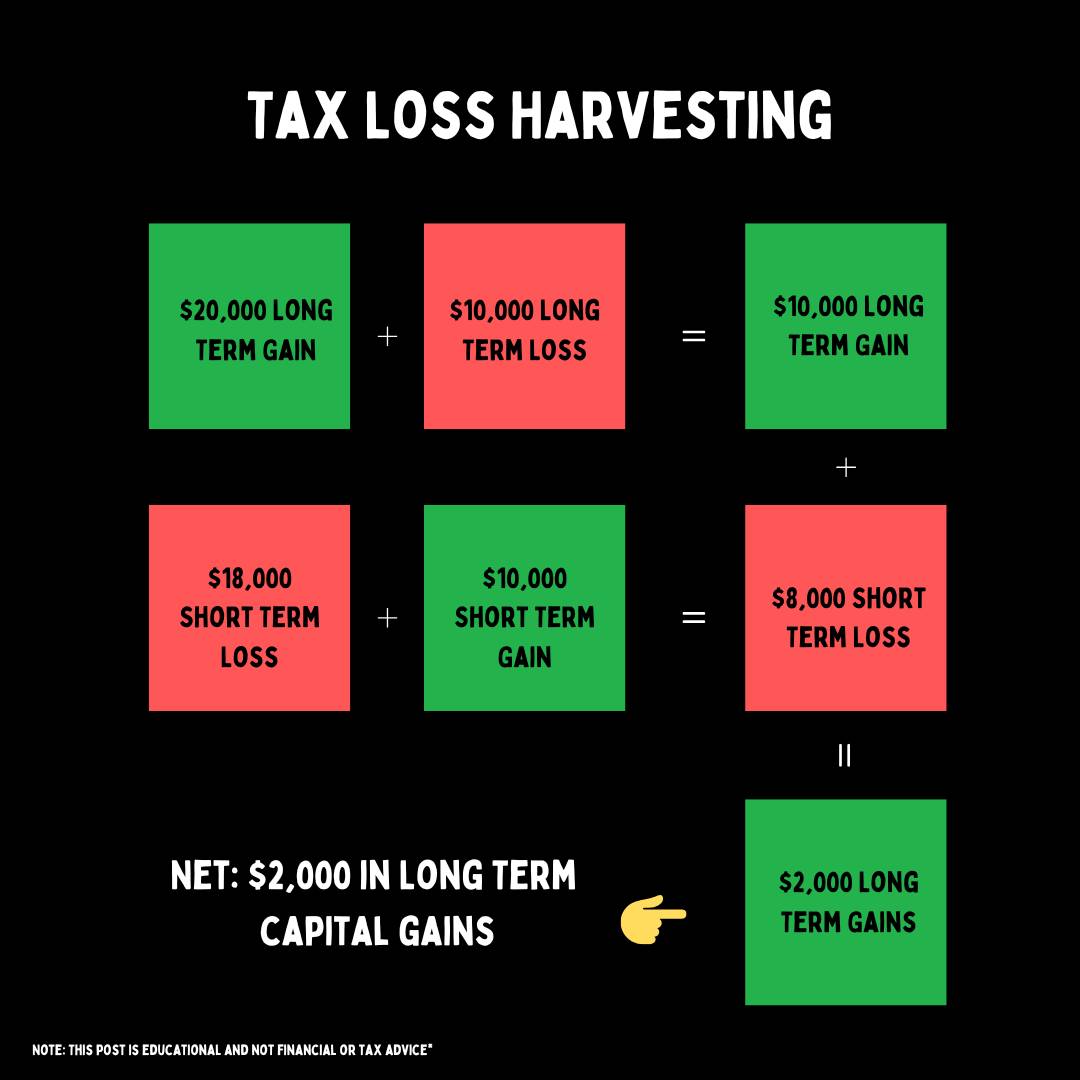

Losses tend to feel like something to avoid, but in reality, they can be one of the most useful tools available. If parts of your portfolio are trading below their cost basis, those losses can be realized and used to offset gains elsewhere. This is especially valuable when you’re trying to unwind a concentrated position.

The key here is that you’re not stepping out of the market entirely. You’re maintaining similar exposure while capturing the loss for tax purposes. Over time, this creates a system where volatility actually works in your favor.

If you have losing positions that you don't want, this is an opportunity to not only potentially reduce your capital gains burden, but even clean up your portfolio by killing two birds with one stone.

Instead of being purely negative, it becomes an opportunity to improve your after-tax outcome while continuing to stay invested.

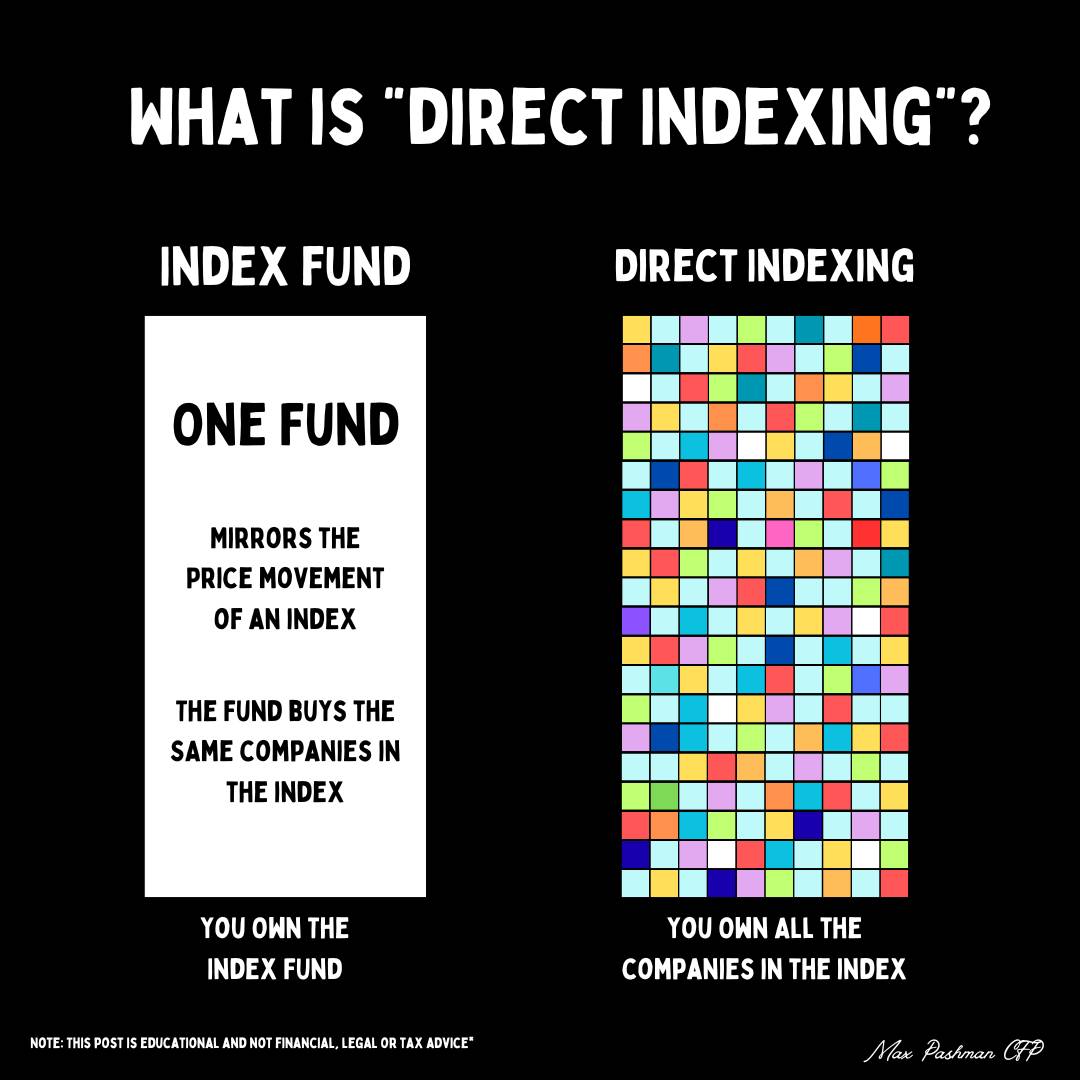

As portfolios grow, there are more opportunities to get precise. Direct indexing takes what is typically a single ETF and breaks it into its underlying holdings. Instead of owning the index as one position, you own the individual stocks inside it.

Why that matters becomes clear in uneven markets. Even when an index is up overall, there are usually dozens or even hundreds of individual stocks that are down. Each of those positions creates an opportunity to harvest losses at a more granular level.

It should be noted that direct indexing is not for everyone. There are costs to manage it, it can complicate your portoflio overall, and these losses over the long run usually are used up within 5-7 years on average. Meaning direct indexing is usually ideal for those who are planning an exit at some point.

Over time, those losses can be used to offset gains from concentrated positions, helping reduce the tax drag that often comes with diversification. It’s not necessary for everyone, but for larger taxable portfolios, it can be a meaningful layer in the strategy.

Sometimes the goal isn’t to realize gains right away, but to delay them.

Exchange funds allow you to contribute a concentrated stock position into a pooled structure and receive a diversified basket in return. The key benefit is that this transition happens without triggering an immediate taxable event. In a way, it’s like swapping out a single position for a diversified portfolio without having to sell.

The tradeoff is that you’re giving up liquidity for a period of time, often several years, and these structures tend to require larger minimums. Because of that, this approach tends to fit specific situations rather than being a default strategy. But when it aligns, it can help reduce concentration while deferring taxes into the future.

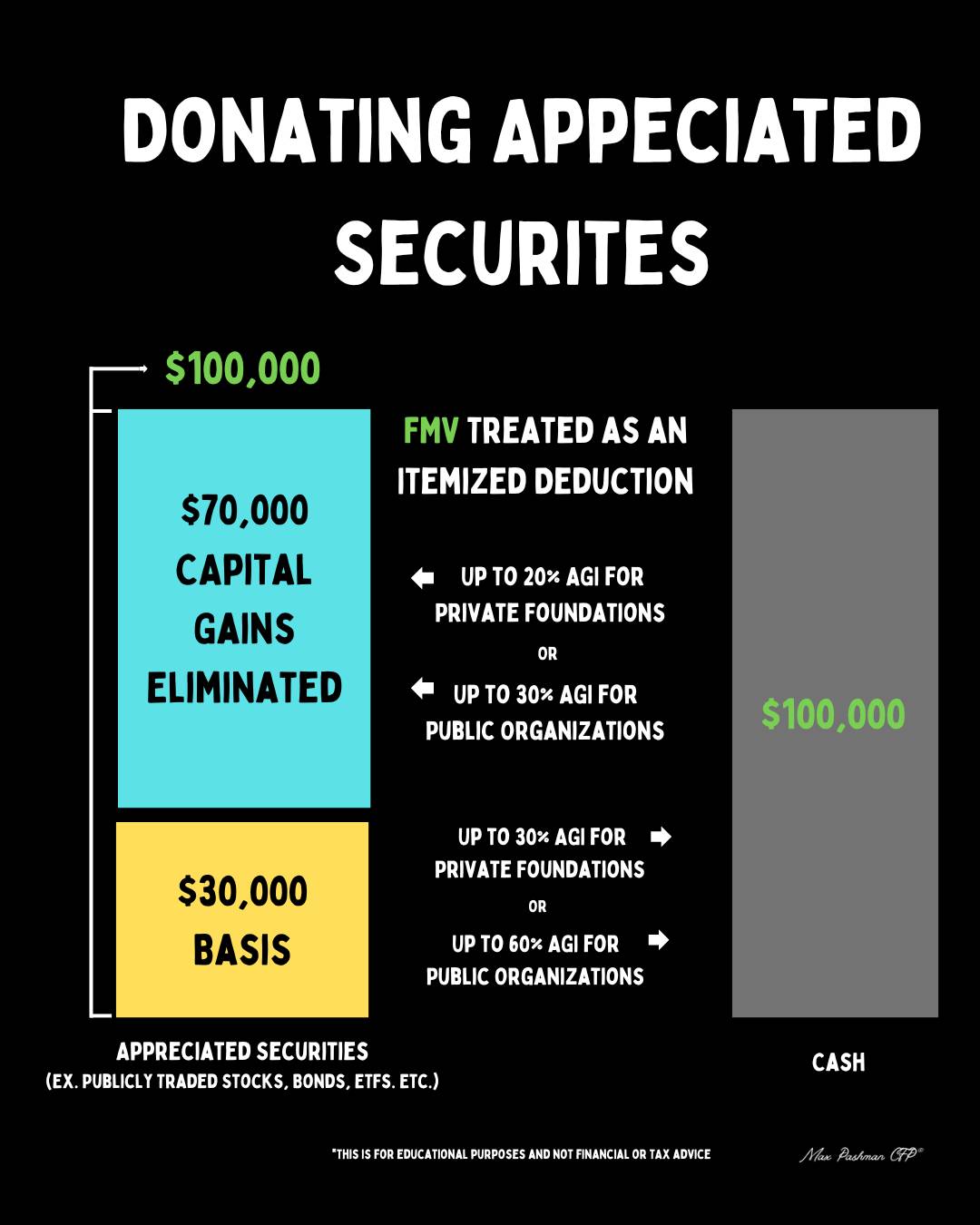

For those who already have charitable intent, concentrated stock can become one of the most efficient assets to give. Donating appreciated shares allows you to avoid realizing the capital gain entirely, while still receiving a charitable deduction based on the value of the stock. Compared to donating cash, the difference in tax impact can be significant.

Structures like donor-advised funds add another layer of flexibility. They allow you to take the deduction in the current year while deciding later where and when the funds are distributed. It turns something you may already want to do into a coordinated planning decision.

There isn’t one perfect solution to concentration.

Most of the time, the right approach is a combination of strategies layered together over time. Some shares are sold gradually, some losses are harvested along the way, and in certain cases, more advanced tools are introduced when appropriate.

The goal isn’t just to diversify. It’s to do it thoughtfully, in a way that balances risk reduction with tax efficiency.

A concentrated position is often how wealth is built. Diversification is how it’s kept.

Need help with your financial planning? Let’s chat and talk more about how we can help elevate your financial situation! Book a call here.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.