Most high earners lose thousands of dollars every year to poor tax planning. Not because they don’t make enough, but because they wait too long to act.

By the time April rolls around, the best tax-saving opportunities are already gone. In fact, year-end is when you still have time to make adjustments that actually matter. Much of what you do now in the coming months can make a massive difference in the next tax season around the corner.

Here are 10 areas to review before December 31st to make sure your money is working as efficiently as possible.

If you have company stock, especially NSOs and ISOs, your tax situation can get complex quickly.

Each type of equity is taxed differently, and decisions made late in the year can dramatically change your tax bill.

Example:

Let’s say your ISOs are deeply in the money. Exercising them in December could trigger AMT (Alternative Minimum Tax), but exercising in January might give you an extra year to hold for long-term capital gains. The amount and timing can make all the diffence.

Similarly, selling RSUs right when they vest might prevent a tax surprise at filing time, since the income was already recognized at vesting.

A good year-end review includes:

Small timing decisions could mean thousands saved in taxes.

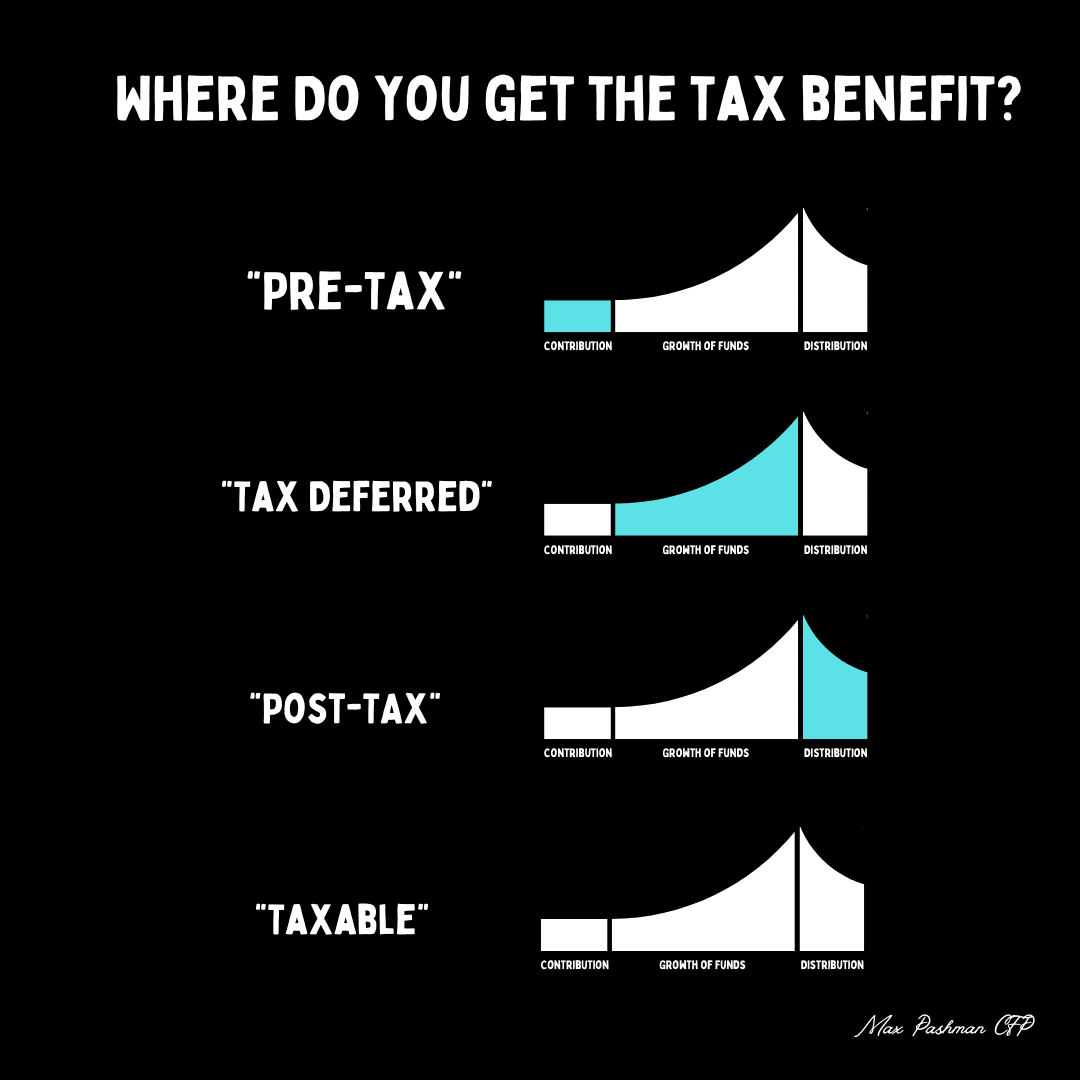

It’s not just about what you invest in, but it’s also where you invest.

Balancing pre-tax, Roth, and taxable accounts gives you control over how much you pay in taxes later on.

Think of these as your three “buckets”:

Example:

Imagine retiring at 55. If all your money is in pre-tax accounts, every dollar you withdraw will be taxed as income. But if you have money in taxable and Roth accounts, you can “mix and match” withdrawals to manage your tax bracket and even qualify for ACA health subsidies or Roth conversions at lower rates.

Tax diversification = flexibility. And flexibility = power.

If you regularly give to charity, you can make those donations go further with some strategy.

Under current law, the standard deduction is high ($29,200 for married couples in 2025), so smaller donations often don’t create a deduction. But “bunching” combining several years of giving into one year can push you over that threshold.

You can also use a Donor-Advised Fund (DAF) to front-load donations now and distribute them over time. If you're an employee who receives equity compensation, this could be an opportunity to not only get an itemized deduction, but also eliminate any long-term capital gains with them too.

Nobody enjoys seeing red in their portfolio, but down markets can create opportunity. Tax-loss harvesting means selling an investment at a loss to offset gains elsewhere.

You can use realized losses to:

Example:

If you sold company stock for a $10,000 gain earlier this year, but another investment is down $10,000 and selling the loser wipes out the gain. Your net tax impact? $0.

Just remember: avoid buying back the same investment within 30 days or you’ll trigger the wash-sale rule, disallowing the loss. Doing this in a timely manner can make all the difference.

Roth conversions turn pre-tax money (Traditional IRA or 401(k)) into Roth money, which then grows tax-free.

They’re especially powerful in low-income or low-valuation years.

Example:

Let’s say you expect to make $100,000 this year instead of your usual $400,000. It could be reasons like an unexpected drop in income, a layoff, or early retirement that requires less income.

Converting $50,000 from your IRA to Roth now means paying taxes at a lower marginal rate, and that new money will grow tax-free now.

HSAs are one of the few triple tax-advantaged accounts available:

Even better there’s no time limit on reimbursements.

Most people contribute to their 401(k) on autopilot, but few stop to ask if they’re using the right type of contribution.

If your income is high now but you expect it to drop later (say, after retiring early or selling your business), pre-tax contributions can make sense.

If you expect your income to rise or tax rates to increase, Roth contributions could be smarter. But having the right strategy is neede to choose one or the other rather than just focusing solely on income.

529 plans are best known for college savings, but they’ve quietly become much more flexible.

Funds grow tax-free, withdrawals for qualified education expenses are tax-free, and starting in 2024, unused 529 funds (held for at least 15 years) can be rolled into a Roth IRA for the beneficiary, up to certain limits with rules to abide by.

Example:

Parents who overfund a 529 can now convert the leftover balance into their child’s Roth IRA later, turning unused education savings into a head start for retirement.

You can also front-load up to 5 years’ worth of contributions ($95,000 per child for couples in 2025) to maximize compounding early. Lump sums could be strategic for that purpose.

Owning property opens the door to multiple tax advantages.

Real estate investors can:

Utilizing these is not a set-and-forget-it situation, as having the right team behind the scenes can make the most of those situations.

The annual gift exclusion for 2025 is $19,000 per recipient.

That means you can give up to $19,000 to as many people as you’d like each year, or $38,000 per person as a couple, without touching your lifetime exemption.

This is a great way to transfer wealth, fund education, or help family members while reducing your taxable estate.

Example:

If you and your spouse gift $38,000 each to two kids every year, that’s $76,000 moved out of your estate annually, completely tax-free.

And with the lifetime exemption at $13.99M (single) / $27.98M (joint) in 2025 set to be cut in half after 2026 strategic gifting can have long-term benefits.

Year-end tax planning isn’t about doing everything. But it’s about knowing which moves apply to you.

For some, that might mean reviewing equity comp. For others, it’s a Roth conversion or a charitable giving strategy.

The earlier you start reviewing, the more tools you have before December 31st.

Which one will you be tackling first?

Need help with your financial planning? Let’s chat and talk more about how we can help elevate your financial situation! Book a call here.

Disclaimer: Pashman Financial LLC, its owners, officers, directors, employees, subsidiaries, service providers, content providers and third-party affiliates referred to as “Pashman Financial” do not offer the sale of securities or other investments. None of the information provided is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Pashman Financial does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Pashman Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained. Please seek the advice of professionals regarding the evaluation of any specific content. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized. The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Pashman Financial LLC (referred to as “Pashman Financial”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Pashman Financial does not warrant that the information will be free from error. None of the information provided on this email and website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Pashman Financial be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if Pashman Financial or a Pashman Financial authorized representative has been advised of the possibility of such damages. In no event shall Pashman Financial LLC have any liability to you for damages, losses, and causes of action for accessing this site. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.