So you’ve heard it a million times: "You can’t touch your 401(k) until you’re 59½". And at first, this is true. But what if I told you there’s a way to get your hands on that money before hitting that age—and do it legally and without the dreaded 10% early withdrawal penalty? Sounds too good to be true, right? Well, it’s not.

Let’s talk about how you can use a little-known strategy to get access to your retirement savings early, penalty-free, and tax-free.

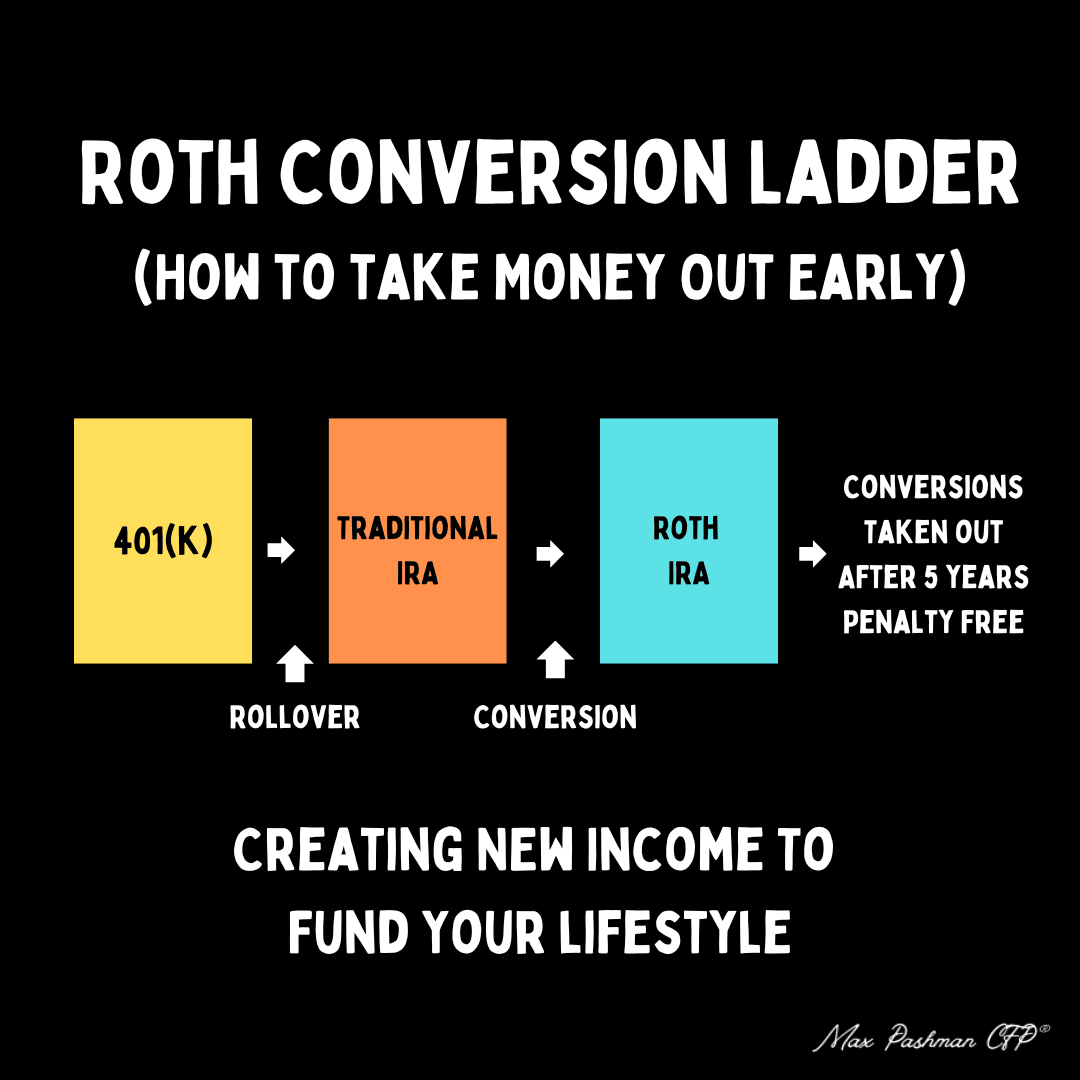

The Roth Conversion Ladder is a multi-step strategy where you move money from a Traditional IRA or 401(k) into a Roth IRA. Here’s the cool part: Once the money is in a Roth IRA, you can withdraw the converted funds tax-free and penalty-free—as long as you follow the rules.

Here’s how it works:

Let’s say you retire at 45 and want to access income before you turn 59½. Here’s how you could use the Roth Conversion Ladder to create a steady, tax-free income stream:

By age 50, you can access your first $50,000, and every year after that, another $50,000 becomes available to you. Over time, you’re building a tax-free income stream without having to wait until you’re 59½.

Why the Roth Conversion Ladder Rocks

Here’s why this strategy is a game-changer:

While the Roth Conversion Ladder is a great strategy, there are a few things to be aware of:

It should also be said this is merely an option, versus the ONLY option for early retirement. Accounts that aren't tax-advantaged, like a taxable brokerage account, are more flexible than this process. This is merely an option to weigh in when factoring every angle

If you’re planning for early retirement or need access to your retirement savings before 59½, the Roth Conversion Ladder is definitely worth considering. It lets you access your money legally, without the early withdrawal penalty and gives you tax-free access once the funds have been converted.

Of course, since this strategy involves some moving parts, it’s a good idea to team up with a financial and tax professional to make sure you’re doing it the right way. But once you’ve got it set up, it’s a fantastic tool for creating a steady income stream for your early retirement years.

Disclaimer: Pashman Financial LLC, its owners, officers, directors, employees, subsidiaries, service providers, content providers and third-party affiliates referred to as “Pashman Financial” do not offer the sale of securities or other investments. None of the information provided is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Pashman Financial does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Pashman Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained. Please seek the advice of professionals regarding the evaluation of any specific content. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized. The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Pashman Financial LLC (referred to as “Pashman Financial”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Pashman Financial does not warrant that the information will be free from error. None of the information provided on this email and website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Pashman Financial be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if Pashman Financial or a Pashman Financial authorized representative has been advised of the possibility of such damages. In no event shall Pashman Financial LLC have any liability to you for damages, losses, and causes of action for accessing this site. Information on this email and website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.