Most people start the same way. They invest in an index fund, stay consistent, and over time… it works. The portfolio grows, the noise fades, and the simplicity becomes the biggest advantage.

Low cost. Broad exposure. Minimal maintenance. It’s one of the few strategies that’s both simple and effective.

But as things progress, a different question starts to come up.

Not just “How is the portfolio doing?”

But “How much of this am I actually keeping after taxes?”

That’s where the conversation begins to shift.

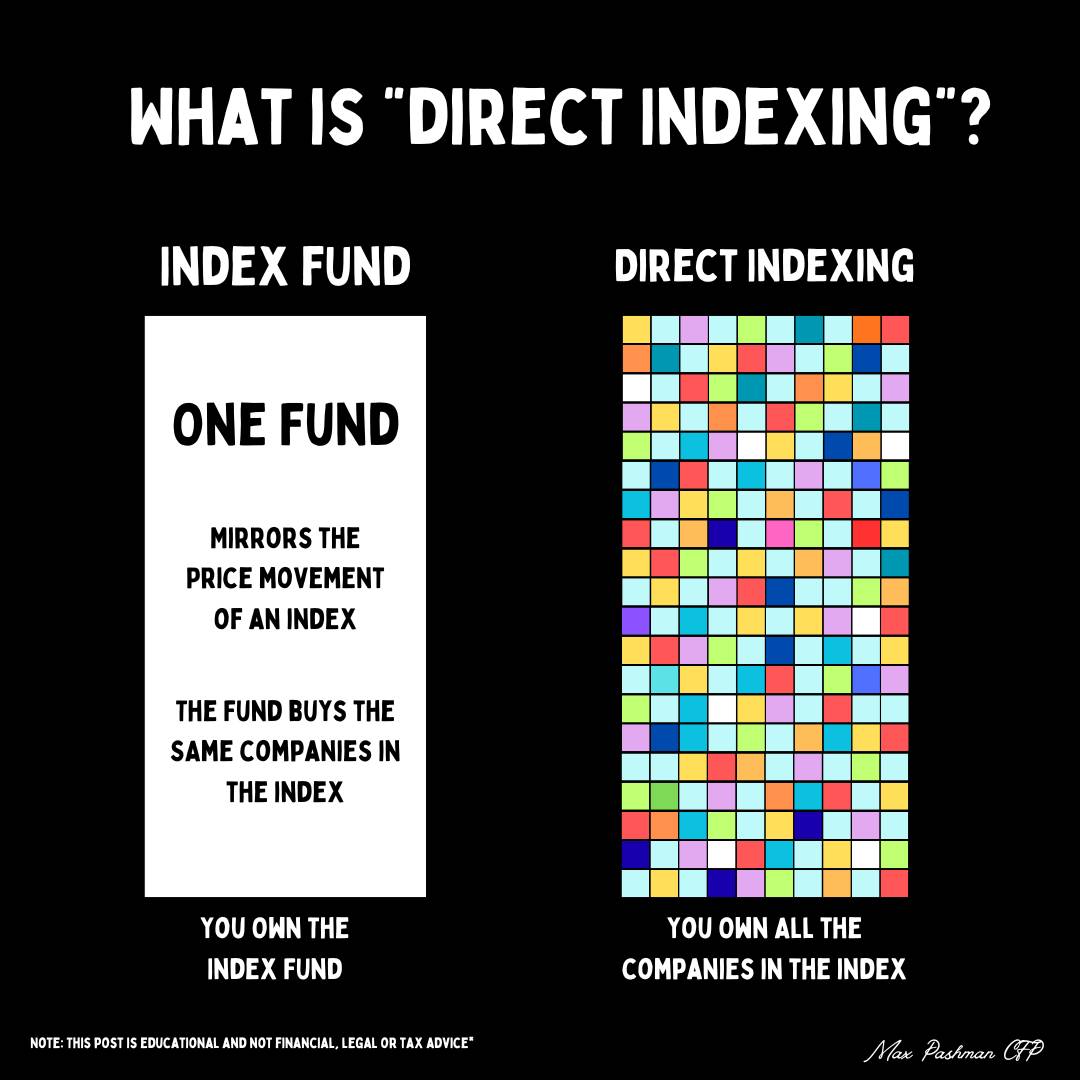

Direct indexing doesn’t change your investment philosophy.

You’re still investing in the market. You’re still tracking an index. You’re still relying on long-term growth.

What changes is the structure underneath it.

Instead of holding a single fund, you hold the individual stocks that make up that fund. From a distance, the portfolio behaves similarly. But under the surface, it becomes much more flexible.

That flexibility is what creates the opportunity.

Traditional index funds are already built with tax efficiency in mind. They do a good job minimizing distributions and allowing gains to compound. But they operate as one position.

That means you don’t have much control over what happens inside the fund. When you own the individual holdings, that changes.

Some stocks will be up. Others will be down. And those differences can be used intentionally.

Losses can be realized and used to offset gains elsewhere, all while keeping your overall exposure relatively intact. Instead of reacting to the market, you’re able to work with it.

Over time, that can lead to a more efficient after-tax outcome, even if the pre-tax returns look very similar.

For smaller portfolios, this level of detail usually isn’t necessary. A simple index fund often does exactly what it’s supposed to do. But as portfolios grow, taxes become a larger part of the equation.

This tends to matter more for those with higher incomes, larger taxable accounts, or ongoing sources of gains. In those cases, even incremental improvements in tax efficiency can compound into meaningful differences over time.

It’s less about doing something completely different and more about refining what’s already working.

This approach isn’t without its costs.

Direct indexing typically comes with an additional fee, and while it may seem small, it adds up over time. There can also be subtle differences between the portfolio and the index, along with small inefficiencies like cash sitting uninvested.

Individually, these may not stand out. Together, they matter.

So the real evaluation isn’t whether the strategy sounds good in theory. It’s whether the after-tax benefit justifies the added complexity and cost.

That being said, fee compression could lower this over time. So it's just a question if the costs justify the benefits as it currently stands. That answer isn’t universal.

One of the biggest factors is how the strategy is introduced.

Trying to shift an existing portfolio into direct indexing often creates a tax event, which can reduce or even eliminate the benefit. Doing so is working backwards. What's the point of moving to a tax strategy if the process potentially negates most of the benefits?

Because of that, this tends to work best when paired with new capital. That could come from income, equity compensation proceeds, or proceeds from a liquidity event. Starting fresh allows the strategy to build without unnecessary friction.

The effectiveness of this approach isn’t static. In more volatile markets, there are more opportunities to capture losses across individual positions. That’s where much of the value tends to come from.

In smoother, upward-trending markets, those opportunities become less frequent. Gains accumulate, and the strategy leans more on deferring taxes rather than actively harvesting losses.

Over time, that shift makes long-term planning even more important.

This is where things can quietly go wrong.

Managing losses isn’t just about one account. It needs to be coordinated across everything you own, including accounts held by a spouse and any overlapping investments.

If that coordination isn’t handled carefully, certain rules can limit or eliminate the intended tax benefit.

The idea itself is straightforward. The execution is where the difference is made.

It’s easy to focus on the immediate benefit of deferring taxes. But eventually, those deferred gains need to be addressed.

That’s why it helps to view this as part of a broader plan. Whether the goal is funding future spending, supporting charitable giving, or passing assets along, the long-term use of the portfolio matters.

Without that context, it’s just a strategy. With it, it becomes part of a plan.

Direct indexing isn’t about replacing what already works. For many investors, a low-cost index fund remains one of the most effective tools available and still completely effective for those who are best qualified for direct indexing.

But for others, especially those with larger taxable portfolios, there may be an opportunity to be more intentional with how taxes are managed over time.

The goal isn’t to outperform the market. It’s to keep more of what the market provides. It always comes down to the proper strategy to justifiy if it works for them.

It’s a way to add another layer of control, particularly around taxes. In the right situation, that can make a meaningful difference over time. In the wrong one, it can simply add complexity without much benefit.

The key is understanding where it fits.

Need help with your financial planning? Let’s chat and talk more about how we can help elevate your financial situation! Book a call here.

You know how to make money, but you're not sure if you're making the right moves financially. That's why I started Pashman Financial.

.png)

PASHMAN FINANCIAL, LLC (“Pashman Financial”) is a registered investment advisor offering advisory services in California and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Pashman Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content on this site is for information purposes only. Opinions expressed herein are solely those of Pashman Financial, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.